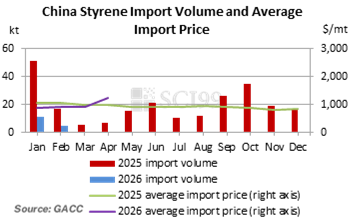

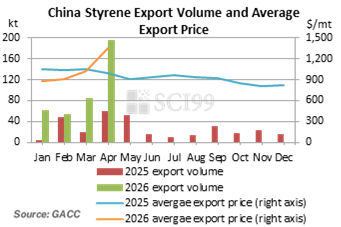

In April 2026, China’s styrene import and export dynamics continued to diverge: Export volume reached 195.4kt, up 231.90% YoY, hitting a new high for the same period in history; meanwhile, Import volume stood at only 0.7kt, plunging 89.64% YoY. This “scissors gap” indicates that China has transformed into a major exporter of styrene.According to data from the GACC, styrene imports in April totaled 0.7kt, an increase of 687.72 mt MoM but a sharp 89.64% decline YoY; the average import price was $1,258.49/mt, down 73.79% MoM but up 25.24% YoY. Cumulative imports from January to April amounted to 17kt, a 79.01% drop compared to the same period last year. Meanwhile, April exports reached 195.4kt, surging 133.19% MoM and 133.19% YoY, marking the highest single-month level on record; the average export price was $1,352.60/mt, up 27.09% MoM and 37.05% YoY. Cumulative exports from January to April totaled 393.4kt, a 202.96% increase YoY

The primary reason for persistently low import volumes in April lies in ample domestic supply and demand. Following profit accumulation during Q1, maintenance schedules for some styrene units have been repeatedly postponed, keeping industry operating rates at relatively high levels (with a monthly average operating rate of 73.90%). At the same time, geopolitical tensions in the Middle East have widened overseas supply gaps, giving domestic prices a competitive edge in the international market. Consequently, downstream enterprises prefer purchasing domestically produced goods over expensive imported alternatives.Due to the small overall import volume, the landscape of import traders in April was highly concentrated. Data shows that nearly all imported supplies originated from Russia, with approximately 687 mt coming from that country, accounting for 99.71% of total imports. This limited batch of imports was entirely handled by companies based in Hebei Province.In April, the exceptionally high level of styrene exports was primarily driven by sudden supply shortages in overseas markets. Affected by geopolitical factors, such as the situation in the Middle East and unexpected shutdowns of overseas units, regions including Japan, South Korea, India, and Europe experienced significant supply gaps. International demand for Chinese styrene remained robust. According to market feedback, contracted order volumes exceeded 200kt in April, with some shipments delayed until May, resulting in export data that fell short of market expectations.In April, India was the primary destination for Chinese styrene exports, accounting for 41.05%, a MoM increase of 14.66 percentage points, followed by South Korea at 22.94%, down 12.63 percentage points from the previous month, and Turkey at 13.19%, a slight MoM decline of 2.07 percentage points. Additionally, Taiwan, Hong Kong, and Japan also exhibited rigid demand, each contributing around 5% of total exports.Exporting enterprises are predominantly concentrated in coastal provinces with well-developed downstream industrial chains. Data show that Zhejiang Province was the front-runner in April, with an export volume of 62.1kt, representing 31.76% of the national total. Shanghai, Jiangsu, and Fujian closely followed, together forming China’s “first-tier” styrene exporters.Looking ahead to May, with unresolved geopolitical issues in the Middle East, China’s styrene trade pattern of “low imports, high exports” is expected to persist.